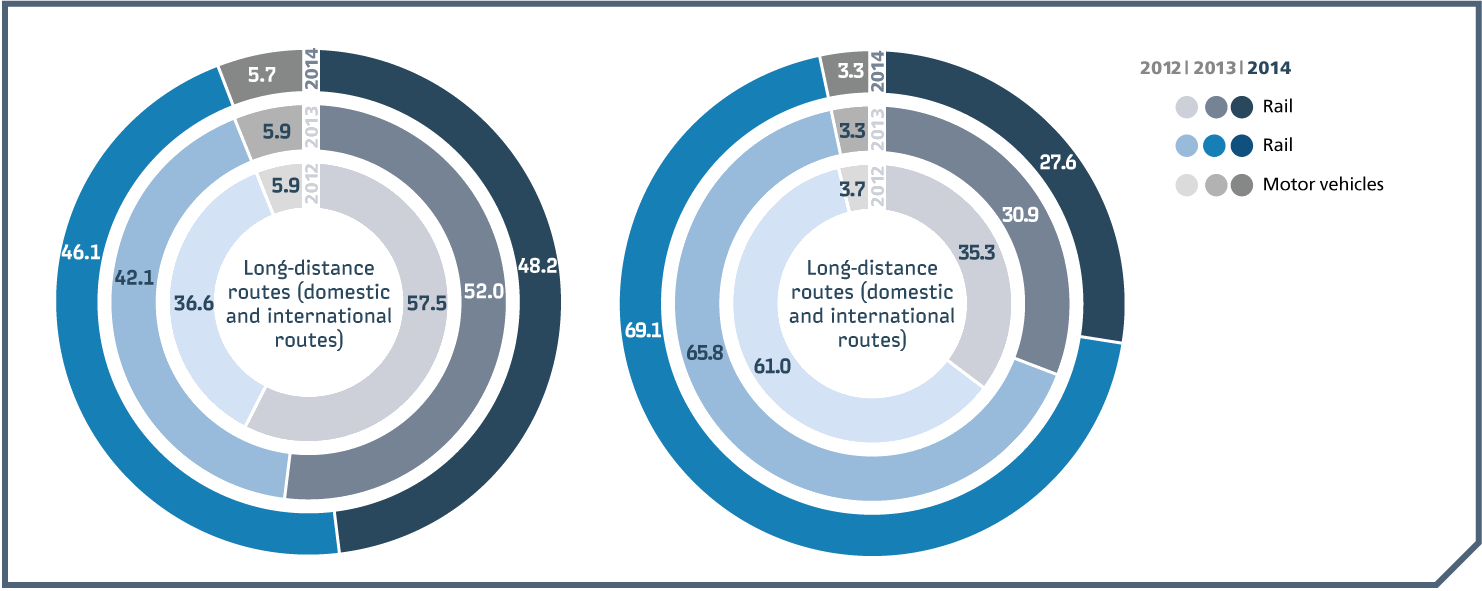

In 2014, the long-distance passenger service market, including domestic and international service, grew by 2.1% to 349.3 billion

One of the forces behind the market expansion was Russia’s civil aviation. So, airlines increased their passenger traffic by 107.2%, while rail companies lost 9% of traffic, which resulted in a change in the transport market structure.

At the end of the reporting year, airlines experienced a decline in passenger numbers on international flights, the key market growth driver over recent years. In the face of growing competition on domestic routes, a high debt burden, weakening rouble and poor financial performance, the companies had to take measures to optimise aircraft supply and improve the efficiency.

As at the end of 2014, rail transport accounted for 27.6% of the long-distance passenger service market, 3.4% down year-on-year.

A similar situation was seen on domestic routes. With the passenger service market growing by 4.1%, the share of rail transport reduced by 3.9%.

The annual reduction of the rail transport’s market share is a sign of a high level of competition in the transport services sector.

Backed by government support, air transport is expanding its domestic presence with subsidised regional flights and allocation of additional funding for air service infrastructure and aircraft fleet.

Among the main competitive advantages of airlines are the speed and, as a consequence, quicker journey times, absence of price regulation and better flexibility in terms of pricing, commercial activities and marketing.

Coach services are another notable competitor, especially for distances of up to 400 km.

Apart from JSC FPC, Russia’s domestic railroad network is currently used by high-speed trains, private carriers’ trains (CJSC Grand Service Express, LLC Tverskoi Express, Megapolis and TransClassService). In addition, JSC FPC has to compete with foreign countries’ railway administrations who offer passenger service to destinations in Russia.

The share of JSC FPC in the domestic passenger service market was 90.1% in 2014 (+1.5 pp vs 2013), while the Directorate for High-Speed Service (DHSS) of RZD accounted for 1.9% (+0.2 p.p. vs 2013). The presence of foreign countries’ railway administrations dropped by 1.8 p.p.

Sources: rail transport — JSC RZD’s reports; air transport — Federal Agency for Air Transport’s data (www.favt.ru); motor transport — JSC FPC’s expert opinion.